August 2024. Quebec is hit hard by the remnants of Hurricane Debby. In just a few hours, torrential rains lead to major flooding and ground movements in several regions, impacting people, buildings and vehicles all at once. It costs just over $2.5 billion in insured damages, prompting the Insurance Bureau of Canada to call this climate event the most expensive one in the history of Quebec.

The scientific link between climate change and the increase in the intensity and frequency of several types of extreme weather events is now recognized.

But what about the connection between climate change and the insurance industry? Let’s take a look at this complex but essential relationship.

What affects the public affects insurance

In the insurance industry, the impacts of extreme weather events are most often associated with home insurance, which covers buildings and physical assets.

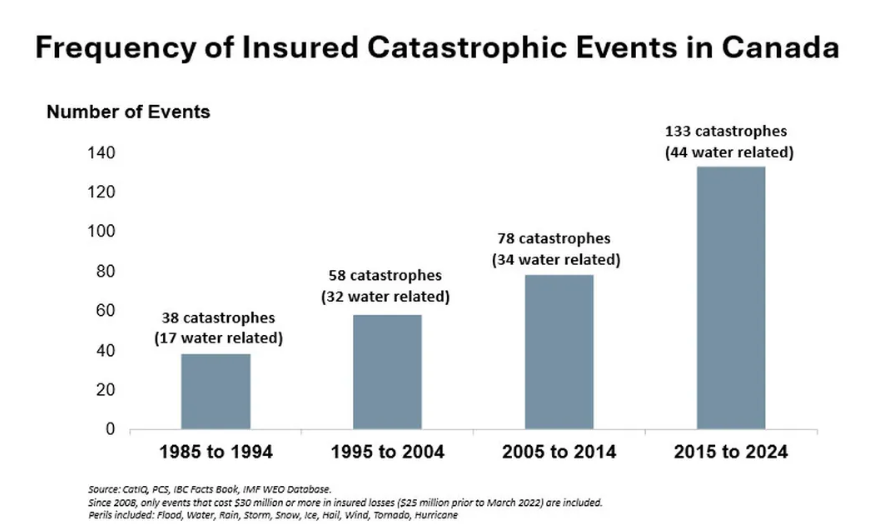

The graph below shows that not only has the frequency of insured disasters increased in Canada since 1985, but a large proportion of them have been water-related. This type of information can guide certain decisions regarding the management of people’s individual protection.

Since the costs associated with climate disasters are piling up, insurers are increasingly engaging in a practice known as “bluelining.” This consists of increasing prices or withdrawing insurance services in areas that are considered to be at high environmental risk. Construction methods and the materials used can also have an impact on insurability.

For example, the vast majority of properties located in flood zones are not covered against flooding, usually because insurance companies are not in a position to protect them at a reasonable cost, without the payouts exceeding the premiums.

In the context of climate change, this situation is becoming not only problematic, but difficult to maintain in the long term.

When insurance becomes an ally in adaptation

Despite the challenges, the insurance industry is also adapting its practices to the effects of climate change.

Following the historic flood in Calgary in 2013, insurers expanded their coverage to include damage caused by river flooding, which was previously non-existent in Canada.

Insurance became an important tool for improving resilience to climate change, with premiums structured so that they encourage owners, businesses and communities to reduce their own exposure.

Flooding in downtown Calgary, June 22, 2013 [Photo: The Canadian Press / Jonathan Hayward]

In fact, several global studies support this trend: in regions where insurance underwriting is more widespread, natural disasters have fewer impacts and communities recover more quickly.

In Quebec...

The Programme général d’assistance financière lors de sinistres (general financial assistance program for disasters) was created to support homeowners and tenants affected by climate events, including floods.

It provides help as a last resort for people who are not covered by an insurance policy. As it is not a substitute for an insurance contract, claimants must communicate with the insurer before applying for financial assistance and compensation.

La Financière Agricole du Québec has developed the programme Assurance récolte (crop insurance program) in response to extreme rain and other hazards affecting the agricultural sector.

This program aims to protect producers from climate risks and uncontrollable natural phenomena, including floods.

Resources available to the public

People have been hearing various terms from their insurers like “exclusions” and “increased premiums”. Faced with the current climate realities, it’s essential that insurers inform everyone about the options available to them.

To raise awareness and better inform the public, the Chambre de l’assurance de dommages du Québec (ChAD) has created a tip sheet [in French] for individual home insurance customers. Among other things, it provides explanations of the types of protection included in a basic home insurance contract and in the addenda covering certain additional losses, such as those caused by water.

Insurance companies are providing some information resources to the public, but they will be called upon to be more and more proactive going forward. The Keep It Intact program offered by Intact Insurance is a good example. In the same vein, the Intact Centre on Climate Adaptation offers relevant infographics that can help people protect their homes.

Insurance coverage for goods and people is a key component of climate change adaptation. The more optimal this protection is, the more it supports the population’s physical and mental security.

What if insurance companies encouraged us, by means of their standards, to improve our personal climate change adaptation? If we want to improve our resilience and our grasp of this poorly understood subject, it’s worth thinking about.